Discover the Best MYGA Rates for Your Investment Needs

Are you looking for a secure way to grow your retirement savings without market risk? A Multi-Year Guaranteed Annuity (MYGA) might be the perfect solution. As a type of fixed annuity, a MYGA offers a simple promise: a guaranteed rate of return for a set number of years. This predictability makes it an excellent tool for retirement planning, allowing you to confidently build your nest egg with a protected principal and a locked-in interest rate.

A multi-year guaranteed annuity, or MYGA, is a straightforward financial product designed for stability. It functions much like a certificate of deposit (CD) from a bank, but it’s offered by an insurance company and comes with unique tax advantages.

With a MYGA, you receive a guaranteed interest rate for a specific term, typically ranging from two to ten years. This means your account value will grow at a predictable pace, shielded from market fluctuations. Let’s explore how these annuities work and what makes them an attractive option.

So, what exactly is a MYGA? Think of it as a contract between you and an issuing insurance company. You make a lump-sum payment, and in return, the company provides a fixed rate of interest for a predetermined number of years. This interest rate is locked in for the entire term specified in your annuity contract.

The process is simple. Once you purchase the MYGA, your money begins to accumulate interest. For example, a 5-year MYGA with a 6.00% rate will earn that exact interest rate each year for five years. This predictability removes the guesswork and volatility associated with other types of investments.

At the end of the term, you have several options. You can renew the contract, transfer your funds into a new annuity, or withdraw your money. This structure provides a secure and reliable way to grow your savings with a guaranteed interest rate.

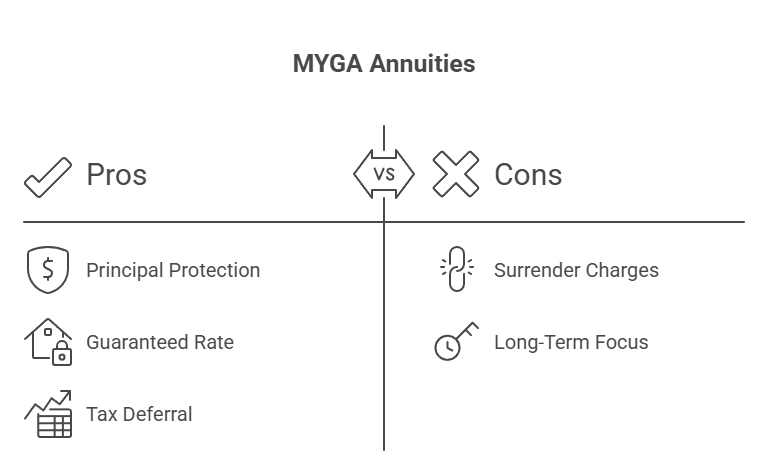

MYGAs stand out due to several appealing features that cater to safety-conscious investors. One of the biggest draws is the combination of security and growth. You know exactly what your return will be, making financial planning much simpler.

These annuities offer significant benefits that protect and grow your money. Key advantages include:

While MYGAs are designed for long-term savings and may have a surrender charge for early withdrawals, they provide a reliable path toward building future retirement income.

Have you ever wondered how insurance companies decide on the annuity rate they offer? It’s not an arbitrary number; several key factors influence the interest rate for a MYGA. The broader economic landscape plays a significant role. When general interest rates and bond yields are high, insurers can offer more attractive rates.

An insurer’s investment strategy and its financial ratings also impact the rates. Companies with very high ratings might offer slightly lower rates in exchange for superior financial stability, while others may offer higher rates to compete for business. Competition among insurers is a major driver of the competitive rates you see in the market.

Additionally, some contracts include a market value adjustment (MVA). This feature can adjust the amount you receive if you withdraw funds before the term ends, based on how prevailing interest rates have changed since you bought the policy.

MYGA annuity products are not one-size-fits-all. They come with various term lengths, giving you the flexibility to choose a guarantee period that aligns with your financial timeline. You can typically select a set period ranging from two to ten years, with some options extending even longer.

Choosing the right term is a key decision in your investment strategy. A shorter term offers more flexibility, while a longer term often secures a higher interest rate. Understanding the different options available will help you make the best choice for your goals.

When you explore MYGAs, you’ll find that a few term lengths are especially popular among investors. These options provide a good balance of yield and flexibility, making them suitable for various financial goals. The annuity rate you receive is often tied to the length of the guarantee period you select.

Generally, the longer you are willing to commit your funds, the higher the fixed interest rate you can lock in. The most common term lengths include:

Each of these terms comes with its own surrender period, which matches the guarantee period. During this time, withdrawals beyond a certain limit may incur a penalty. This structure encourages long-term saving while providing a clear timeline for when your funds will be fully accessible.

Choosing a term length for your annuity contract depends on your specific needs. Shorter terms offer quicker access to your full account value, while longer terms typically provide a higher interest rate, leading to more growth.

Understanding the trade-offs can help you decide. A 3-year MYGA is great for short-term goals, whereas a 7-year MYGA is better suited for money you won’t need to touch for a while. The 5-year option often represents a “sweet spot” for many investors, balancing a competitive interest rate with a moderate time commitment.

Here is a simple breakdown of the differences:

| Feature | 3-year MYGA | 5-year MYGA | 7-year MYGA |

|---|---|---|---|

| Best for | Short-term goals, laddering strategies | Balancing yield and flexibility | Long-term savings, maximizing rate |

| Interest rate | Generally lower | Often the sweet spot | Typically higher |

| Flexibility | Higher, funds accessible sooner | Moderate | Lower, funds locked in longer |

Selecting the ideal MYGA duration is a personal decision that should align with your financial goals. Start by considering when you might need access to your money. If you are building retirement savings and have a long time horizon, a 7- or 10-year term could maximize your growth potential.

For conservative investors who are closer to retirement or may need the funds sooner, a shorter 3- or 5-year term might be more appropriate. This approach provides stability without locking up your investment amount for too long. It allows you to reassess your strategy in a few years as market conditions change.

Ultimately, the right choice connects your timeline to your objectives. Think about what you want to achieve with this portion of your portfolio—whether it’s preserving capital, generating steady growth, or setting aside funds for a future purchase—and pick the term that best supports that goal.

Finding the best MYGA rates requires a look at the current market. Rates are dynamic and can change based on economic trends and competition among insurance companies. Right now, MYGA rates are among the highest they have been in over a decade, making it an excellent time to consider this investment.

To ensure you get the most competitive offer, it is essential to compare current rates from multiple providers. Different companies will have different offerings, so shopping around is the key to maximizing your return.

As you search for the highest MYGA rates in 2026, the best place to start is online. Many financial websites and independent insurance brokerages offer quoting engines that compare the best rates from numerous carriers in one place. These tools are updated regularly to reflect changing market conditions.

When comparing rates, remember that the highest number isn’t the only factor. You should also verify the financial strength of the insurance company offering the rate. Look for providers with strong ratings from agencies like A.M. Best. To find the best options for you:

These steps will help you identify top-tier products that offer both attractive rates and long-term security.

Comparing rates from various insurance companies is a critical step in securing the best deal. You will notice that rates can differ significantly from one provider to another, even for the same term length. This is due to differences in company strategy, investment performance, and financial stability.

A simple way to compare is to create a table that lists the key details for each option. Pay close attention to the A.M. Best rating, as this indicates the insurer’s ability to meet its financial obligations. A higher rating provides greater peace of mind.

Here’s a sample comparison of competitive rates from different companies:

| Insurance company | Term | Rate | A.M. Best rating |

|---|---|---|---|

| Knighthead Life | 7 years | 6.50% | A- |

| Wichita National Life | 5 years | 6.15% | B+ |

| Mountain Life | 7 years | 5.80% | B |

| Americo Financial | 5 years | 5.50% | A |

| Clear Spring Life | 5 years | 5.40% | A- |

When you search for current rates online, you will likely encounter both “live rate feeds” and opportunities to get a “quoted offer.” It’s important to understand the difference. A live rate feed displayed on a web browser shows the general top rates available in the market at that moment.

However, the rate you ultimately receive might be different. A quoted rate is a personalized offer based on your specific details. Factors that influence your final quote include:

Think of a live rate feed as a starting point. To get an accurate picture of what you can earn, you need to submit your information to receive a formal annuity quote. This ensures the rate you see is the rate you will actually get.

While a high interest rate is appealing, the financial strength of the insurance company behind the annuity is just as important. The guarantees of a MYGA are backed by the claims-paying ability of the insurer. Therefore, choosing a company with strong financial ratings is essential for your long-term security.

Independent agencies provide a credit rating for each insurance company, offering a clear measure of their financial stability. Before committing to a MYGA, you should always review these ratings to ensure your investment is in safe hands.

Insurer ratings are a critical indicator of an insurance company’s health and its ability to fulfill its promises to policyholders. When you purchase a MYGA, you are trusting the issuing insurance company to protect your principal and pay the guaranteed interest over the entire guarantee period.

Financial strength ratings from agencies like A.M. Best give you an objective assessment of this ability. A company with a superior rating (such as ‘A++’ or ‘A+’) has demonstrated a strong track record of financial stability and prudent management. This means there is a very high likelihood it will be able to meet its obligations for years to come.

Choosing an insurer with a lower rating might get you a slightly higher interest rate, but it comes with increased risk. For a product designed for safety, prioritizing a company with strong financial strength ratings is a wise decision.

The annuity market in the United States features many reputable life insurance company providers known for their financial stability and competitive rates. While the top rate leaders can change frequently, certain names consistently appear with strong offers and solid financial backing.

These companies have a long history of serving customers and maintaining robust balance sheets. When shopping for a MYGA, you’ll likely come across a mix of well-known brands and some smaller, highly competitive firms.

Here are a few examples of companies that often provide attractive MYGA options:

Always verify the current rates and ratings for any company you are considering, as market positions can shift.

Verifying an insurer’s financial stability is a straightforward but necessary step. You don’t have to be a financial expert to do it. Independent rating agencies do the heavy lifting for you by analyzing each company’s financial health and assigning a simple credit rating.

The most prominent rating agency for the insurance industry is A.M. Best, which uses a letter grade scale from A++ (Superior) down to D (Poor). It is generally recommended to stick with companies that have a rating of ‘A-‘ or better. To check a company’s financial strength, you can:

Taking a few minutes to do this research provides an essential layer of protection for your investment.

MYGA rates are not set in a vacuum. They are influenced by a variety of economic forces, much like other financial products. The prevailing interest rate environment is the most significant driver, meaning rates will rise and fall with broader market conditions.

Understanding these factors can help you gauge whether it’s a good time to buy. When you see rates climbing, it is often due to wider economic trends and increased competition among insurers, creating opportunities for savers to lock in higher yields without market volatility.

Several major economic trends directly affect the interest rate environment and, consequently, MYGA rates. Insurance companies invest the premiums they receive, primarily in high-quality bonds. The returns on these bonds heavily influence the rates they can offer on their annuity products.

In an environment of rising interest rates, such as those driven by Federal Reserve policy changes, insurers can earn more on their investments. They pass these higher earnings on to consumers in the form of more attractive MYGA rates. This makes MYGAs a popular choice for retirement planning when rates are high.

Key economic factors include:

These elements of the financial markets shape the landscape for fixed-income products like MYGAs.

Beyond broad economic trends, factors specific to each insurance company also play a crucial role in setting MYGA rates. Each insurer has its own business strategy and risk tolerance, which affects how aggressively it prices its products. Some companies may aim to lead the market with the highest rates to attract a large volume of new business.

Others may adopt a more conservative approach, offering slightly lower but still competitive rates while emphasizing their superior financial strength. This competition among insurance companies is great for you as a consumer, as it pushes providers to offer better terms and more attractive yields.

A company’s current portfolio performance and its need for new capital can also influence short-term rate specials. This is why you might see one company’s rates jump ahead of others for a brief period before the market adjusts.

Two of the most direct factors you can control that affect your MYGA rate are the term length and your investment amount. Insurers often reward investors who are willing to commit their funds for a longer period. A 7-year annuity contract will almost always offer a higher rate than a 3-year contract from the same company.

Similarly, the size of your deposit can make a difference. Some insurance companies have rate tiers, meaning a larger investment amount might qualify you for a higher interest rate. For example, an investment of $100,000 could receive a better rate than an investment of $25,000.

When you get a quote, these two details are essential for determining the final rate. A larger deposit held for a longer term generally results in a higher guaranteed interest rate, leading to a greater final account value.

When you are looking for a safe place to put your money, a fixed annuity isn’t your only choice. It is helpful to compare MYGAs with other popular fixed-income options like a bank CD (certificates of deposit) or a bond. Each of these has its own set of features, benefits, and drawbacks.

By understanding how MYGAs stack up against these alternatives, you can make a more informed decision about which product best fits your needs for safety, growth, and tax efficiency.

It’s useful to know the difference between a MYGA and what’s known as a traditional fixed annuity. Both offer a guaranteed rate, but the structure of that guarantee is different. A MYGA guarantees the same annuity rate for the entire term of the contract, whether it’s 3, 5, or 7 years.

A traditional fixed annuity, on the other hand, typically guarantees an initial rate for only the first year. After that, the insurer declares a new rate each year. While this new rate will not fall below a specified minimum, it can fluctuate, making your returns less predictable than with a MYGA.

For investors who prioritize certainty and want to know exactly what their retirement income or savings will grow to, a MYGA is often the better choice. Its locked-in rate removes any uncertainty about future returns during the term.

MYGAs, certificates of deposit (CDs), and bonds are all considered safe havens for capital, but they have key differences. A bank CD is perhaps the most similar to a MYGA, offering a fixed interest rate for a set term. However, MYGAs often come out ahead in a few areas.

MYGAs frequently offer higher interest rates than CDs of a comparable term. More importantly, the interest earned in a MYGA grows tax-deferred, while the interest from a CD is taxed as ordinary income each year. This tax advantage allows your money to compound faster in a MYGA.

Here is a quick comparison:

Looking ahead to 2026, which safe investment is likely to offer the best return? While market conditions can always change, MYGAs are currently positioned to outperform many comparable bank CDs and bonds, especially when considering their tax advantages.

The growth potential of a MYGA is enhanced by its tax-deferred status. Because you don’t pay taxes on the interest until you withdraw it, more of your money stays invested and continues to earn interest. This can lead to a significantly higher net return over time compared to a taxable investment like a CD, even if the headline interest rates are similar.

For long-term retirement savings, this tax-deferred compounding gives MYGAs a powerful edge. If current market conditions hold, a MYGA is likely to be one of the highest-yielding, low-risk options available for growing your money.

Once you’ve decided that a MYGA is right for you, the next step is to secure the best MYGA rates available. This involves a bit of timing and a clear process for comparing your options. Locking in a high guaranteed rate can make a substantial difference in the long-term growth of your lump sum investment.

By following a few simple steps, you can confidently navigate the process and ensure your annuity contract provides the optimal return for your financial situation.

Timing can play a significant role in maximizing your returns from a MYGA. Since interest rates fluctuate, making your purchase when rates are at a peak can lock in a higher yield for the entire term of your contract. Currently, rates are at multi-year highs, making it an opportune time to buy.

Is it possible to lock in a MYGA rate before it changes? Yes. The interest rate is secured when your application is signed and received by the insurance company. This protects you if rates happen to drop while your application is being processed. To time your purchase effectively:

By locking in a favorable rate, you ensure your money benefits from a higher level of compound interest, which is key for building future retirement income.

Getting an accurate rate for a MYGA is a straightforward process. While you can see general rates online, a personalized annuity quote will reflect the offer available to you based on your specific circumstances. This ensures there are no surprises down the line.

To get started, you’ll need to provide some basic information, including your state of residence, age, and planned investment amount. A financial advisor or an online annuity marketplace can then generate quotes from multiple insurance companies for you to compare.

Here are the simple steps to follow:

This process empowers you to find the most competitive and accurate rate for your needs.

The application process for a MYGA is typically simple and can often be completed online. Insurance companies have streamlined their procedures to make it easy for you to secure your annuity. Good customer service from the provider or your agent can help guide you through each step.

While it’s not complicated, the application does require you to provide specific information and make sure all details are accurate. Understanding what’s needed beforehand can help ensure the process goes smoothly from start to finish.

When you are ready to complete a MYGA application, you will need to have several pieces of information on hand. The insurance company requires these details to issue the annuity contract, confirm your identity, and ensure the product is suitable for your financial situation. A financial advisor can help you gather everything you need.

The application will ask for standard personal and financial details. Being prepared with this information will make the process quick and efficient, usually taking only 15-30 minutes to complete.

You will typically need to provide:

Buying a MYGA is a significant financial decision, and avoiding common pitfalls can help ensure it meets your expectations. One of the most important things to be aware of is the surrender charge period. MYGAs are long-term products, and withdrawing more than the allowed amount before the term ends will result in penalties.

Before signing the annuity contract, make sure it aligns perfectly with your financial goals. A mismatched product can lead to frustration if you need access to your funds unexpectedly or if the term is too long for your timeline. To avoid mistakes:

By keeping these points in mind, you can select a MYGA that provides stability without causing future inconvenience.

While MYGAs are designed for long-term growth, insurance companies understand that you may need access to your funds. Most annuity contracts include provisions for withdrawals, but it’s crucial to understand the rules to avoid unexpected fees. Early withdrawals beyond the free withdrawal amount will typically trigger a surrender charge.

These penalties are in place to allow the insurance company to manage its long-term investments that back your guaranteed rate. Knowing the specific terms of your contract regarding withdrawals, surrenders, and penalties will help you manage your investment wisely and avoid costly surprises.

The rules for early withdrawals are a key feature of any MYGA contract. If you take out more money than the penalty-free amount during the surrender period, the insurance company will assess a surrender charge. This fee is typically a percentage of the amount withdrawn and declines each year until it reaches zero at the end of the term.

For example, a 5-year MYGA might have a surrender charge that starts at 9% in the first year and drops by 1-2% each year thereafter. Additionally, some contracts include a market value adjustment (MVA).

It is essential to review these details in your contract so you know exactly what to expect if you need to access your funds before the surrender period is over.

Even with surrender charges, most MYGAs offer flexible withdrawal options that allow you to access a portion of your account value without penalty. These provisions are designed to give you some liquidity while your money continues to grow.

A common feature is a free withdrawal provision, which often allows you to take out up to 10% of your annuity’s value each year. Some contracts may also permit you to withdraw the interest earned without incurring a charge. These options give you a way to create an income stream or cover small, unexpected expenses.

It’s important to remember that these withdrawals may still be subject to income tax on the gains and an IRS penalty if you are under age 59½. Always check your specific contract for the details on your available withdrawal options.

In conclusion, understanding and comparing MYGA rates is essential for making informed investment decisions. By grasping the key features and benefits of Multi-Year Guaranteed Annuities, you can better navigate your options and secure a financial strategy that aligns with your goals. Keep in mind the various factors that influence MYGA rates, including term lengths and economic trends. As you explore the current market snapshot, remember to assess the financial strength of the insurers you’re considering. If you’re ready to take the next step, get a free consultation to discuss how MYGAs can fit into your investment strategy and help you achieve financial security.

MYGA rates are not static; they can change at any time based on shifting market conditions and the current interest rate environment. An insurance company may adjust its rates weekly or even monthly to stay competitive and respond to changes in bond yields. It’s always best to confirm the current rate when you apply.

Yes, you can lock in a guaranteed rate. The rate for your annuity contract is secured at the time of your purchase, specifically when the issuing insurance company receives your signed application and funds. This protects you from any downward rate adjustments that might occur during the policy-issuing process.

To compare competitive rates, use an online quoting tool in your web browser to see offers side-by-side. Look at the interest rate, term length, and, most importantly, the insurer’s financial strength rating. A financial advisor can also provide a detailed comparison of annuity contract options from various providers.

This content is provided for informational purposes only and does not constitute financial, legal, or insurance advice. We do not guarantee the accuracy or completeness of this information. All decisions should be made in consultation with a licensed professional who can evaluate your specific circumstances. Product availability and terms may vary by state and individual eligibility.

Key Highlights Introduction Thinking about your future is a huge part of smart retirement planning. Your IRA annuity is a valuable piece of your retirement plan, but what happens if you need it to cover long term care costs? It’s a common question with a complex answer. Using these funds is possible, but it involves […]

In This Article: Our annuity calculator guide will help you understand which inputs matter, how to interpret the projected values, and where misleading assumptions can distort the outcome. A multi-year guaranteed annuity calculator can make retirement projections feel straightforward at first glance. Enter a premium amount, choose a contract term, plug in an interest rate, […]

Key Highlights Introduction Are you looking for ways to ensure your money lasts throughout your retirement? A key part of retirement planning is creating a reliable source of retirement income that gives you financial security. While Social Security and pensions are common income sources, annuities offer another powerful tool. Specifically, an annuity with an income […]