Understanding how does an indexed annuity differ from a fixed annuity is key to making the right choice for your financial future. Fixed annuities provide guaranteed returns and stability, while indexed annuities offer principal protection with the potential for higher returns tied to market performance. This article explores these differences to help you choose the best option for your investment strategy.

Key Takeaways

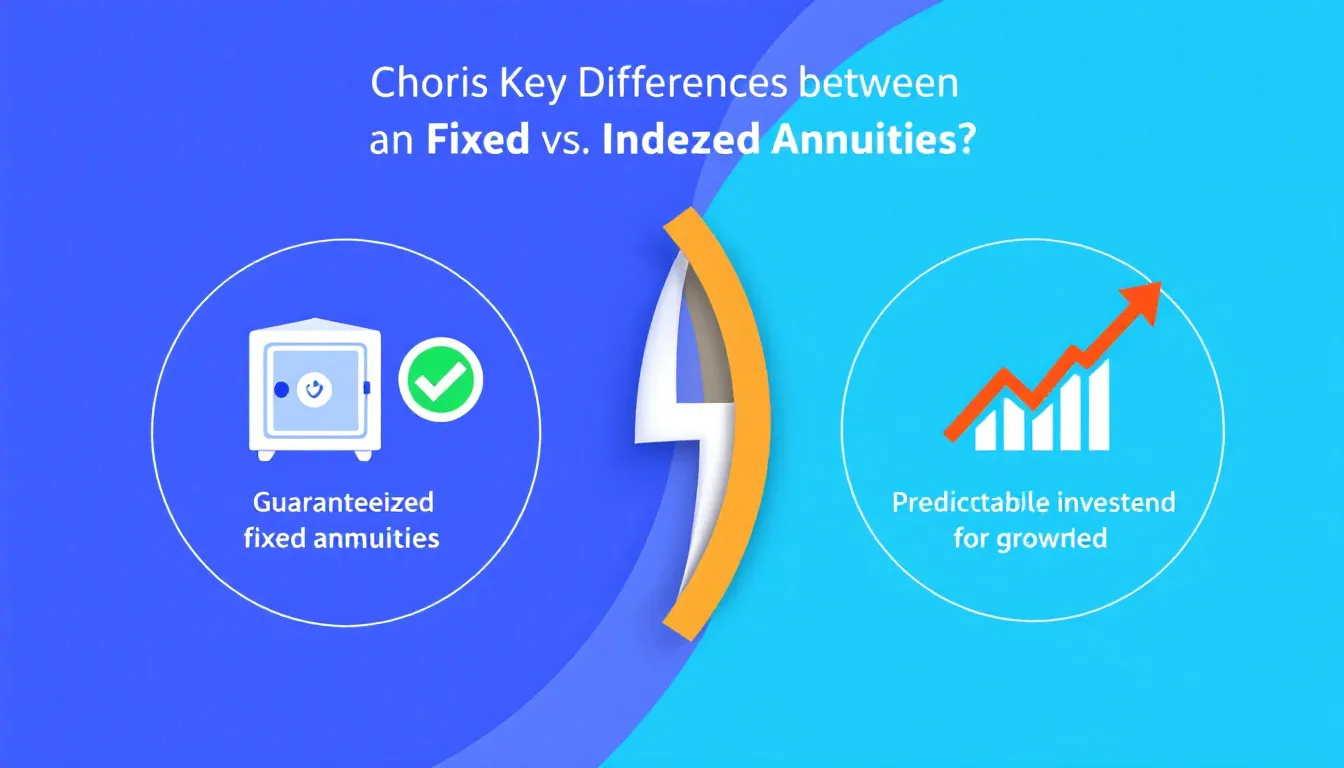

- Fixed annuities provide stability and guaranteed returns, appealing to conservative investors, while indexed annuities offer growth potential linked to market performance with principal protection.

- The interest rate mechanism is a key differentiator; fixed annuities guarantee stable rates, whereas indexed annuities offer variable returns based on market indices.

- Choosing the right annuity should align with individual financial goals and risk tolerance, with fixed annuities suitable for low-risk preferences and indexed annuities catering to those seeking potential higher returns.

Understanding Fixed Annuities

Fixed annuities are a cornerstone of conservative investment strategies. These annuity contracts guarantee both the principal and a rate of return on investment, providing stability and predictable income. They are not subject to the whims of stock market volatility, relying instead on the financial strength of the insurance company. This makes them particularly appealing to individuals entering or preparing for retirement who prioritize conservative investment options, including deferred annuity, fixed and variable annuities.

The primary allure of fixed annuities lies in their ability to offer a steady, lifetime monthly income. Investors seeking peace of mind and predictable returns often gravitate towards these products. However, while they pose minimal risk and guarantee returns, there’s a caveat: fixed annuities may not keep pace with inflation, potentially eroding purchasing power over time.

Guaranteed Interest Rate

A guaranteed interest rate is one of the most appealing aspects of a fixed annuity. This feature:

- Ensures a stable return on investment

- Provides predictable growth regardless of market conditions

- Has predetermined interest rates that remain unchanged for the duration of the contract, typically ranging from 3% to 6%, offering a minimum guaranteed interest rate, credit interest, guaranteed income, a guaranteed income stream, and a guaranteed percentage.

This stability allows savvy investors to plan their finances with confidence, knowing exactly what returns they can expect.

Moreover, these annuities typically guarantee a minimum growth rate, often around 2%, ensuring some level of return even in less favorable economic climates. The guarantee periods for these fixed rates can vary, generally lasting from 2 to 10 years, providing flexibility to match different financial planning horizons.

Types of Fixed Annuities

Fixed annuities come in several types, each offering unique features to cater to different investment needs. Traditional fixed annuities provide:

- A guaranteed minimum interest rate that remains consistent throughout the contract term

- Appeal to those seeking predictability and security

- A straightforward structure, with the insurer guaranteeing both the interest rate and the return of principal.

On the other hand, Multi-Year Guarantee Annuities (MYGAs) offer guaranteed interest rates over multiple years. They provide stability and security similar to traditional fixed annuities but with the added advantage of locking in rates for a specified period, which can be particularly beneficial during periods of fluctuating interest rates.

Exploring Indexed Annuities

Indexed annuities present a unique blend of security and growth potential. These annuities combine the principal protection of a fixed annuity with the opportunity for higher returns linked to stock market indices, including equity indexed annuity options and fixed indexed annuities, as well as fixed index annuities. This means that while your principal is safeguarded, your returns can benefit from favorable market conditions, providing a balanced approach to growth and security, including how indexed annuities can enhance your financial strategy.

The primary characteristic of an indexed annuity is its ability to offer growth potential while protecting against market downturns. This balance makes indexed annuities appealing to investors who are looking for a middle ground between the safety of fixed annuities and the growth potential of more volatile investments.

Market Index Linkage

The performance of indexed annuities is directly tied to a specific stock market index. This means that the interest accrued is a reflection of how well these indices perform. Changes in a specified market index determine how interest is credited, making the returns variable and dependent on market performance.

When the market performs well, indexed annuities tend to outperform fixed annuities, offering potentially higher returns and market gains, despite the uncertainty introduced by market fluctuations compared to the guaranteed rates of fixed annuities.

Despite this variability, the potential for higher returns can make indexed annuities an attractive option for those willing to accept some market-linked risk.

Principal Protection

One of the most compelling features of indexed annuities is principal protection. This ensures that your initial investment remains intact regardless of market performance. Essentially, even if the market performs poorly, your principal is safeguarded, and you won’t lose your initial investment.

In cases where the market declines, indexed annuities typically yield no interest but also do not result in any loss of principal. This downside protection makes them a safer alternative to direct stock market investments, offering a blend of growth potential and security.

Key Differences Between Fixed and Indexed Annuities

Understanding the key differences between fixed and indexed annuities is crucial for making an informed decision. Fixed annuities prioritize stability and predictability, making them suitable for conservative investors seeking guaranteed returns. In contrast, indexed annuities offer potentially higher returns, especially in favorable market conditions, while still providing principal protection.

The choice between these two types of annuities depends largely on individual financial goals and risk tolerance. By examining the interest rate mechanisms, earnings potential, and risk protection features, investors can better align their annuity choices with their financial objectives.

Interest Rate Mechanism

The interest rate mechanism is a fundamental difference between fixed and indexed annuities. Fixed annuities:

- Provide stable and guaranteed interest rates throughout the contract term, ensuring certainty of returns.

- Grow at a guaranteed rate specified in the annuity contract.

- Offer predictable income.

On the other hand, indexed annuities tie their interest rates to market indices, making them variable and dependent on market performance. Although they often include a guaranteed minimum interest rate, typically between 1 to 3 percent, the actual returns can fluctuate based on how well the market performs. This variability introduces a different dynamic compared to the fixed rate annuities’ stability.

Earnings Potential

Earnings potential is another critical aspect where fixed and indexed annuities differ. Fixed annuities typically offer lower earning potential with stable returns, making them suitable for conservative investors. These annuities provide a predictable income stream and can contribute to interest earnings, which is particularly beneficial for retirement planning.

Indexed annuities, however, offer the potential for higher returns due to their link to market performance. While this can lead to greater earnings, the growth potential is often capped by specific rate caps and participation rates, which define the maximum returns possible. This means that while indexed annuities can outperform fixed annuities in a good market, their returns are still somewhat limited.

Risk and Protection

Both fixed and indexed annuities offer principal protection, ensuring that investors do not lose their initial contributions. Fixed annuities:

- Provide minimal risk through guaranteed returns

- Are a safer choice for risk-averse investors

- Ensure that the principal investment is protected

- Offer predictable returns

Indexed annuities, while also offering principal protection, involve moderate risk due to their dependence on market performance. This means that while the principal is protected, the returns can vary, introducing some level of risk. Overall, fixed annuities are safer with guaranteed returns, whereas indexed annuities provide a balance of potential higher returns with market-linked risk exposure.

Costs and Fees

Understanding the costs and fees associated with annuities is essential for evaluating their overall value and effectiveness. Indexed annuities typically have more varied fees compared to fixed annuities. These can include administrative fees, surrender charges, and other costs that can impact the overall returns.

Being aware of these costs can significantly affect long-term financial outcomes. Investors need to carefully consider and compare the fees associated with each type of annuity to make informed decisions that align with their financial goals.

Administrative Fees

Administrative fees are a crucial aspect to consider when evaluating annuities. Fixed annuities generally have lower administrative fees compared to indexed annuities. This is because indexed annuities often include additional features that require higher administrative costs.

Investors should carefully evaluate the administrative fees associated with indexed annuities, as these fees can impact the overall investment performance and returns. Understanding these fees helps in making a more informed decision about which type of annuity to choose.

Surrender Charges

Surrender charges apply for early withdrawals in both fixed and indexed annuities. Typically, these charges decrease over time, making funds more accessible as the annuity contract matures. This gradual reduction in surrender charges and surrender periods can lead investors to incur surrender charges, which can be an essential factor for investors considering the liquidity of their investments.

Indexed annuities may provide options for penalty-free withdrawals, typically allowing up to 10% of the contract value to be withdrawn without incurring surrender charges. However, tax deferred early withdrawals from annuities can also incur harsh IRS penalties, adding to the risk of illiquidity.

Choosing the Right Annuity Based on Financial Goals

Choosing the right annuity involves aligning the annuity choice with your financial goals, risk tolerance, retirement savings, and retirement planning needs, including considerations for retirement age. Annuities can provide a reliable income stream during retirement, but it’s crucial to consider your specific needs and goals when selecting an annuity.

Carefully considering individual financial goals is crucial. Factors like risk tolerance and investment horizon should also be taken into account. Consulting with a financial professional can also help tailor the choice to your unique circumstances.

Assessing Risk Tolerance

Evaluating your risk tolerance is essential when selecting the right annuity for your financial goals. Fixed annuities are a suitable choice for those who favor low-risk investments with guaranteed returns. These annuities provide peace of mind with their predictable income streams.

For individuals with a higher risk tolerance, indexed annuities may be more appealing due to their potential for greater returns linked to market performance. However, it’s important to remember that these annuities carry slightly higher risk compared to fixed annuities.

Matching Retirement Goals

Aligning your retirement income requirements with the features of different annuities is crucial for ensuring financial stability during retirement. Fixed annuities are suitable for covering known fixed expenses due to their guaranteed payments and stability. They provide a reliable income stream and income payments that can help manage daily living costs.

Indexed annuities, on the other hand, provide the potential for higher monthly income as they can be influenced by market performance and interest rate variations. By strategically using both fixed and indexed annuities, investors can ensure a reliable income stream in retirement, balancing stability with growth potential. Understanding how indexed annuity work can enhance your financial strategy is crucial.

Summary

In summary, understanding the differences between fixed and indexed annuities is essential for making informed financial decisions. Fixed annuities offer stability and guaranteed returns, making them ideal for conservative investors. Indexed annuities, while providing principal protection, offer the potential for higher returns linked to market performance, suiting those with a higher risk tolerance.

By carefully considering your financial goals, risk tolerance, and retirement needs, you can choose the annuity that best fits your situation. Consulting with a financial professional can further help in tailoring your annuity choice to ensure a secure and prosperous retirement. Make informed decisions today to build a financially secure tomorrow.

Frequently Asked Questions

What are the main differences between fixed and indexed annuities?

The primary distinction between fixed and indexed annuities is in their interest rate structures; fixed annuities guarantee a stable interest rate and consistent income, whereas indexed annuities are linked to stock market indices, allowing for potentially higher returns with greater variability.

How does the principal protection in indexed annuities work?

Principal protection in indexed annuities guarantees that your initial investment remains secure, ensuring that you do not lose your principal even during market downturns. This feature allows you to benefit from market gains without risking your original capital.

What are the typical fees associated with indexed annuities?

The typical fees associated with indexed annuities include higher administrative fees and surrender charges for early withdrawals, which can significantly affect overall returns. Therefore, it is crucial to carefully assess these fees before investing.

How should I choose between a fixed annuity and an indexed annuity?

Choose a fixed annuity if you prioritize stability and a guaranteed return, while an indexed annuity may be more appropriate if you seek growth linked to market performance and can tolerate some volatility. Your decision should reflect your financial goals and risk tolerance.

Can I withdraw money from my annuity before retirement without penalties?

You can withdraw money from your annuity before retirement, but typically, early withdrawals incur surrender charges. Some indexed annuities may allow penalty-free withdrawals up to 10% of the contract value, though you should also consider potential IRS penalties.